A common point of contention in fraud cases focuses on one important word: material. The defense attorneys say a false statement made by the defendant didn’t matter because it wasn’t material. It wasn’t important enough, or it didn’t really change things, or the bank didn’t rely on it, or the rules were unclear. That argument often gives defendants room to claim confusion or mistake.

But in the case of Letitia James and her alleged mortgage fraud, the contract itself may close that door.

The Second Home Rider she signed in August 2020 defines the word material for us. It says, plainly, that false statements about occupancy are material by definition. That single clause could make it difficult for any defense team to argue that the alleged misrepresentations were immaterial or unintentional.

What “Material” Really Means

In federal fraud statutes, materiality generally refers to the importance of a statement to the decision-making process of a party to a transaction and how the statement might influence the outcome of a situation.

Under 18 U.S.C. § 1014 for loan applications, however, prosecutors do not need to prove that a lender relied on a false statement or suffered financial loss. All they need to show is that the borrower knowingly made the false statement for the purpose of influencing the bank.

Most fraud cases turn on whether a statement by the defendant mattered. A defense attorney might argue that the bank would have made the same loan even if it had known the truth. But that kind of defense in this case likely will not work, because it doesn’t matter what the lender would have done if Letitia James had told the truth in her mortgage application. All that matters under the law is whether she lied.

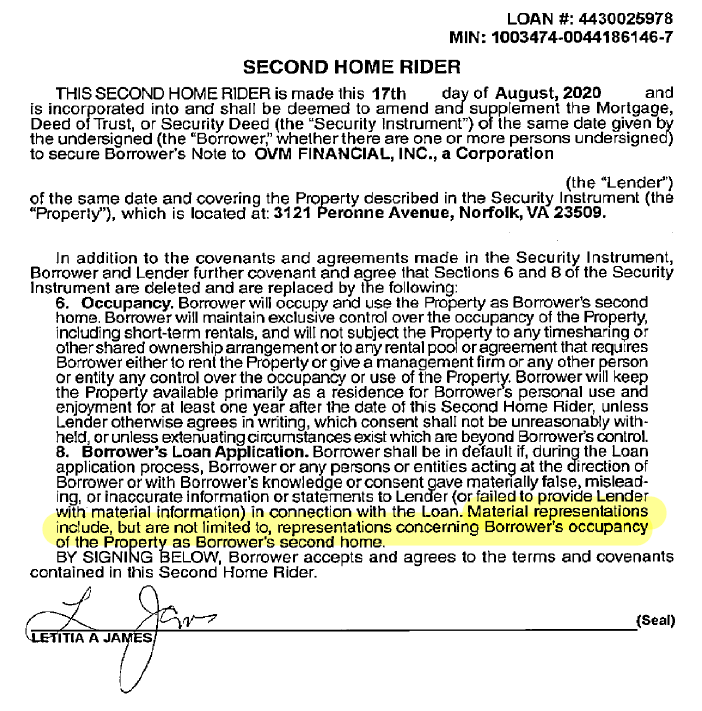

The Crime Defined in the Second Home Rider

The Second Home Rider attached to James’s Norfolk, Virginia mortgage includes a section titled “Borrower’s Loan Application.” It reads:

Borrower shall be in default if, during the Loan application process, Borrower or any persons or entities acting at the direction of Borrower or with Borrower’s knowledge or consent gave materially false, misleading, or inaccurate information or statements to Lender (or failed to provide Lender with material information) in connection with the Loan. Material representations include, but are not limited to, representations concerning Borrower’s occupancy of the Property as Borrower’s second home.

This language eliminates ambiguity. It doesn’t matter whether a jury thinks occupancy rules are unclear or whether the lender actually verified usage. It doesn’t matter if the jury thinks what Letitia James said about the occupancy is important or not. The borrower agreed in this contract that occupancy representations are material.

By signing the rider, James acknowledged that any false or misleading statement about how she would use the property would constitute default. That means she also acknowledged the significance of the statement. The contract itself creates the materiality standard the government must meet.

Why This Undermines the “Weak Case” Narrative

Some commentators have argued that the government’s case against James is “dangerously weak” or based on “squishy” mortgage rules. But this clause undercuts that argument. The relevant standard isn’t found in Fannie Mae guidelines or internal lender policies. It’s in the contract the borrower signed.

If the prosecution can show that James certified she would “occupy and use” the Norfolk property as her second home but she never did, they can win. She agreed that occupancy representations were material, and she agreed that false ones would constitute default.

Intent and Knowledge

Materiality is only part of what the government must prove. Intent is the other critical element. Prosecutors will argue that James’s actions show she knew her statements were false when she made them. Sam Antar does another deep-dive into the conflicting statements Letitia James made to different entities:

- She declared to the lender in August 2020 that she would occupy the Norfolk property as her second home.

- She told her insurance company in August 2020 it would be “owner-occupied non-seasonal use,” meaning she would live there year-round.

- James never occupied or used the Norfolk home. Instead, Nakia Thompson and her children moved into the home in August 2020.

- Thompson testified to a grand jury that she paid no rent for the house. However, according to the indictment, on James’s Schedule E to her personal tax return, she reported “zero personal use days” and reported thousands of dollars of rent received as well as deductions for expenses related to the property.

These conflicts easily prove mortgage fraud, tax fraud, or both because all of the statements Letitia James made can’t possibly be true. Further this pattern of dishonesty can help prosecutors establish intent. A single inconsistency might be explained away. Repeated contradictions, especially across sworn documents, suggest deliberate conduct. James will have a hard time arguing that this was just a mistake when the dishonestly happens repeatedly.

Why the Contract Matters So Much

Fraud investigators will tell you that documents don’t lie. In this case, the documents speak even louder because they define a very specific term… one that is often a point of contention.. The Second Home Rider doesn’t leave materiality to legal interpretation. It puts the borrower on notice that lying about occupancy is a material misrepresentation.

That makes the prosecution’s job simpler. They don’t have to rely on expert witnesses or industry standards. They can point to the borrower’s own signature beneath a paragraph that labels occupancy representations as material and defines false ones as default.

It also limits the available defenses. Claiming the language was unclear or the mistake was small doesn’t work when the contract spells out that the issue is significant. Claiming the misrepresentation didn’t influence the lender’s decision doesn’t work when the borrower agreed it was material regardless of influence.

In the Letitia James case, prosecutors will still need to show that she knowingly made false statements for the purpose of influencing a financial institution. But unlike many fraud cases, they don’t have to fight about whether those statements mattered. She already agreed that they did.

When a borrower signs a document defining a false statement as material, the contract itself becomes a piece of evidence. And in this case, it may be one of the most compelling pieces the prosecution has.

Source link